Blogs

October 10, 2017 Kelley Reeser, R.D. L.D.N. C.D.E.

Decoding Medicare Advantage Plans: Illinois Resources Included

Making sense of Medicare isn’t easy. Parts, A, B, C, D; HMOs; PFFS plans; SNPs. Navigating the system can feel like learning to code… blindfolded… with one hand tied behind your back. The point is, it can be overwhelmingly complicated. But at MD at Home one of our goals is to make quality healthcare easier to access and understand, so in this post we’re decoding the ins and outs of Medicare Advantage Plans, from A to Z.

What is a Medicare Advantage Plan?

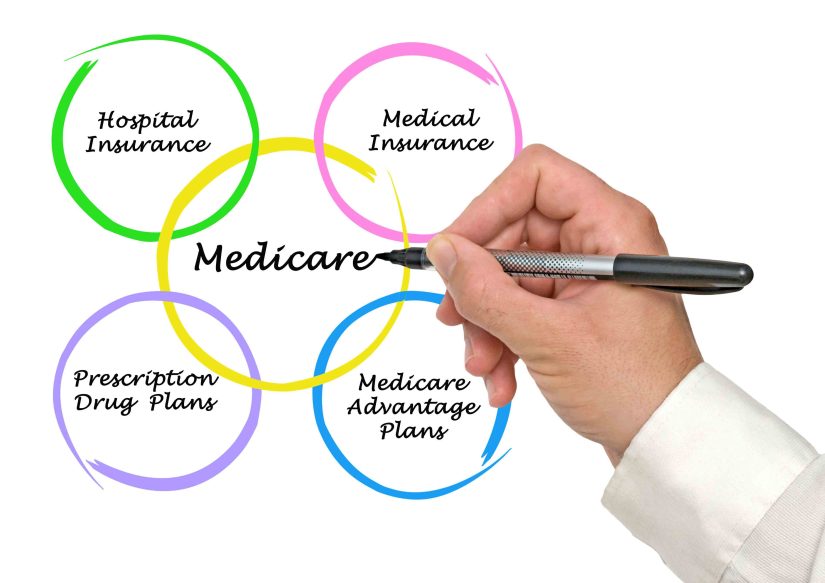

Let’s start with the basics: Medicare is the government-run health-insurance plan for people age 65 and older, people under age 65 with disabilities, and people with End-Stage Renal Disease (ESRD).

Medicare consists of four main parts.

Medicare Part A (Hospital Insurance)

Part A covers inpatient hospital stays, care in a skilled nursing facility, hospice care, and some home health care.

Medicare Part B (Medical Insurance)

Part B covers certain doctors’ services, outpatient care, medical supplies, and preventive services.

Medicare Part C (Medicare Advantage Plans *BINGO, our topic for today)

This is a type of Medicare health plan offered by a third-party private company that, in cooperation with Medicare, can provide you with all the benefits of Part A and Part B. Many Medicare Advantage Plans also offer prescription drug coverage.

Medicare Part D (Prescription Drug Coverage)

Part D plans cover the cost of prescription drugs for which Original Medicare alone doesn’t pay and is offered through private Medicare-approved insurance companies.

Together, Parts A & B are often referred to as “Original Medicare.” When you Medicare Advantage Plan (Medicare Part C).

Different Types of Medicare Advantage Plans

There are several types of Medicare Advantage Plans including:

Health Maintenance Organization (HMO) Plans

With an HMO Plan you receive your health care services from doctors, health care providers, and hospitals within the plan’s network (with the exception of emergency care, out-of-area urgent care, and out-of-area dialysis).

Preferred Provider Organization (PPO) Plans

With a PPO Plan you pay less if you use doctors, hospitals, and other health care providers within the plan’s network. You pay more if you use doctors, hospitals, and providers outside of the network.

Private Fee-for-Service (PFFS) Plans

With a PFFS Plan, the plan determines how much it will pay doctors, other health care providers, and hospitals, and how much you will need to pay when you get care.

Special Needs Plans (SNPs)

SNPs limit membership to people with specific diseases or characteristics, so unless you fit the profile, you won’t be able to join an SNP. Medicare SNPs tailor their benefits, provider choices, and drug formularies to best meet the specific needs of the groups they serve.

Medical Savings Account (MSA) Plans

With an MSA Plan, Medicare deposits money into a bank account, you can then use this account to pay for your healthcare services throughout the year (with a high deductible). The plan gives you full flexibility in choosing your health care services and providers.

There are a few key differences between Medicare Advantage Plans. Let’s take a look.

How to Choose a Medicare Advantage Plan (especially useful for residents of Illinois)

Not all Medicare Advantage Plans work the same way, so before you sign up for one, take the time to compare plans in your area. For Illinois residents, we’ve gathered up a few useful resources including:

- A comparison of the Best Illinois Medicare Advantage Plans;

- A roundup of 2018 Medicare Advantage Plans available in Illinois; and

- A Medicare Supplement Premium Comparison Guide provided by the Government of Illinois.

Before deciding on a plan be sure to ask three important questions:

- What is my share of the costs for services and supplies?

- Does the plan have a network of providers for some or all categories of services?

- Does the plan offer benefits not covered by Original Medicare (e.g. vision, hearing, dental, or prescription drug coverage)?

Still unsure? Try Medicare’s Plan Finder or speak to someone at 1-800-MEDICARE.

How to Join a Medicare Advantage Plan

Once you’ve decided on a provider, joining a Medicare Advantage Plan is as easy as 1, 2, 3 (just make sure you’re signing up during the appropriate time of year as there are specific times when you can enrol in these plans or make changes to coverage you already have – for more on eligible enrollment times visit medicare.gov).

How to enroll:

Visit the plan’s website to see if you can sign up online or contact the plan to get a hard copy enrollment form. Complete the enrollment form (either online or on paper).Contact Medicare 1-800-MEDICARE to complete enrollment. You’ll be asked to provide your Medicare number and the date your Part A and/or Part B coverage started (this info can be found on your Medicare card).

Medicare can feel overwhelming but it doesn’t have to be. Taking the time to research different options and find the plan that best suits your needs will save you thehassle and heartache down the road. There’s not a one-size-fits-all solution, but with a little time and effort, you’ll find a plan that’s just right.

For more information on Medicare, or to learn more about our collaborative, proactive, and preventative approach to patient health, visit MD-athome.com, the premier healthcare resource for homebound patients in Chicago and the Chicagoland area.